Guest post by The Financial Library

We all know the college stereotypes. You have the math and science nerds, the jocks, the frat bros, and many more. But there is only common bond that many of college kids share. And that bond is frugality. Between the late night ramen noodles or the inexpensive adult beverages we drank, we all had at least 1 frugal habit throughout college.

Some of these frugal habits can actually have long lasting impacts on your spending habits post-graduation. Some of them being not very healthy or maybe not the best for us. The problem, for most, is the lifestyle inflation as the average person has a salary of just over $50,000 right out of college. They get that first paycheck that is probably more money than what they are used to and they want to blow that money. You want the new car, the new clothes, or the latest iPhone. But what would happen if you stayed on a budget that was somewhat similar to your college lifestyle with minimal lifestyle creep? What impact would it have on your long term wealth?

Let’s take the example of John. In college John worked part time throughout the school year and had some sort of full-time employment during the summers. Overall, he made $20,000 each year throughout college but because he has living and college related expenses, he spends that $20,000 in full.

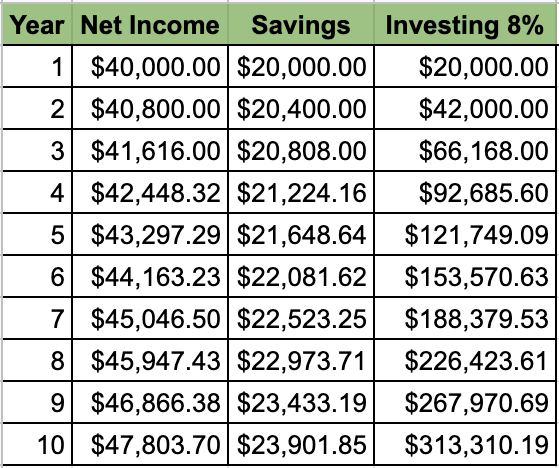

But the four years of college go by for John and he graduates with a degree in business. He gets a job and makes what is equivalent to what the average salary of a college graduate makes: $50,556. But as we all know, Uncle Sam takes his cut of around 20%. So now John has $40,000 left over to spend on whatever he wants. But let’s say that he sticks to the same or a very similar budget to what he had in college and still spends $20,000 per year on living expenses. The remaining $20,000 goes towards investing. We will also be assuming that John’s expenses and salary will rise by 2% per year in this example and the following examples. We will also assume that the average yearly return on his investments is 8% per year. We are also assuming that he makes a lump sum deposit into his investment at the end of the year.

So, assuming his expenses start at $20,000 and rise 2% per year and his post-tax salary starts at $40,000 and rises at 2% per year, John will have a net worth of $313,310.19 at the end of 10 years. What makes this just as crazy as it sounds is that this is nearly $115,000 more than what the average person has in his/her 401(k) ($198,600), according to Nerd Wallet… in their 60’s, when most are considering retiring!

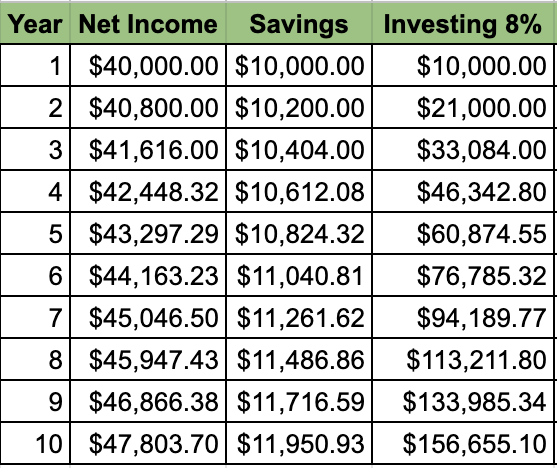

But let’s compare this to a situation where John spends $30,000 on various living expenses and he saves the rest. We will also assume the same other assumptions above, the only 2 differences being, he spends $30,000 and invests the difference ($10,000 in this case). Because John’s savings is half of what it is in the prior example, after 10 years, his net worth is half of what it is above, $156,655.10 but is still not bad.

But let’s take this a step further and assume a savings rate that is closer to what most people actually do, invest right around 10% of his/her pre-tax income. In this case, that works out to be $5,000 for John. In this scenario, this is 25% less than the first example as you can see below.

Now what if we stretch this out to 30 years? What are the consequences over that period of time as most individuals invest for usually 20-40 years before they retire? For the John that started by investing $20,000 of his income, he ends up with about $2.75 million. In the second example, where he started investing half of that, he ends up about $1.375 million. And in the last example, where he saves about 10% of his gross income, he ends up with about $687,000. In all three scenarios, he makes out pretty well but the difference between the first and the third example is a staggering $2.062 million!

Now I understand that in all of these examples, I made many assumptions. Some of those can include, but are not limited to, John not having any debt (or at least not mentioning it) in any of the examples, not including any other sort of savings goals most should have such as an emergency fund and/or saving for a home, investing for 30 years as opposed to 40 if he started at 22 years old and retired at 62, not having any money whatsoever after college, and assuming that nothing crazy happens to his financial picture such as getting injured and not having the ability to work again.

But overall, regardless of what your budget was in college, in most instances, it was probably less than what it was post college and I can guess that it will have an impact on most people’s net worth. As cliche as it may sound, budgeting your money can have some serious consequences.

Hope you enjoyed this article and if you want more content such as this, visit The Financial Library for more!